1st PUC Business Studies Question and Answer Karnataka State Board Syllabus

1st PUC Business Studies Chapter 1

Nature and Purpose of Business

Scroll Down to Download Nature and Purpose of Business PDF

Multiple Choice Questions: Nature and Purpose of Business

Question 1.

Which of the following does not characterise business activity?

(a) Production of goods and services

(b) Presence of risk

(c) Sale or exchange of goods and services

(d) Salary or wages

Answer:

(d) Salary or wages

Question 2.

Which of the broad categories of industries covers oil refineries and sugar mills?

(a) Primary

(b) Secondary

(c) Tertiary

(d) None of them

Answer:

(b) Secondary

Question 3.

Which of the following cannot be classified as an auxiliary to trade?

(a) Mining

(b) Insurance

(c) Warehousing

(d) Transport

Answer:

(a) Mining

Question 4.

The occupation in which people work for others and receive remuneration in return is known as:

(a) Business

(b) Employment

(c) Profession

(d) None of them

Answer:

(b) Employment

Question 5.

The industries that provide support services to other industries are known as:

(a) Primary industries

(b) Secondary industries

(c) Commercial industries

(d) Tertiary industries

Answer:

(d) Tertiary industries

Question 6.

Which of the following cannot be classified as an objective of a business?

(a) Investment

(b) Productivity

(c) Innovation

(d) Profit earning

Answer:

(a) Investment

Question 7.

Business risk is least likely to arise due to:

(a) Changes in government policy

(b) Good management

(c) Employee dishonesty

(d) Power failure

Answer:

(b) Good management

Short Answer Questions: Nature and Purpose of Business

Question 1.

State the Different types of economic activities.

Answer:

Economic Activities are actions undertaken to earn a living and involve the production, exchange, and distribution of goods and services to generate income. These activities are essential for acquiring wealth and meeting basic human needs such as food, clothing, and shelter. For instance, a businessman earns profits through commerce, a doctor receives fees for medical services, and an employee earns wages or salaries for their work. Economic activities are crucial for satisfying human needs by producing and distributing goods and services.

Types of Economic Activities

Economic activities can be broadly classified into three main categories:

1. Business:

Engaging in the production, distribution, and sale of goods and services regularly to earn profits.

Example: A retailer selling clothing, a manufacturer producing machinery, or a service provider offering digital solutions. Business activities focus on generating money and wealth through economic transactions.

2. Profession:

Activities that require specialized knowledge and skills are often regulated by professional bodies and characterized by a high level of expertise.

Example: Chartered accountants, doctors, and lawyers. Professionals offer specialized services based on their expertise and qualifications.

3.Employment:

Working for others in exchange for wages or salaries creates a contractual relationship between the employer and the employee.

Example: A factory worker, a salesperson, or a manager. Employment involves performing tasks or services as part of an organisation or business entity in return for compensation.

Question 2.

Why is business considered an economic activity?

Answer:

Business is considered an economic activity because it involves the production and sale of goods and services with the primary goal of earning a profit by fulfilling human needs in society. Unlike activities driven by emotions such as love, affection, or sympathy, business is specifically undertaken to generate income or a livelihood. Its main focus is on financial gain rather than sentimental reasons.

Question 3.

Explain the Concept of Business.

Answer:

Concept of Business

Business refers to an organized effort to provide goods and services to society, primarily driven by the goal of earning profit.

• B.O. Wheeler defines business as an institution operated to supply goods and services to society with the incentive of private gain.

• L.H. Haney describes business as a human activity aimed at producing or acquiring wealth through the buying and selling of goods.

• Peterson and Plowman explain business as an activity where individuals exchange something of value, whether goods or services, for mutual gain or profit.

In practice, business encompasses various economic activities related to the production, distribution, trading, or exchange of goods and services to meet the needs of people and earn income or profit. It involves activities such as manufacturing, trading, transportation, insurance, warehousing, banking, and finance, covering the entire spectrum of commerce and industry.

Question 4.

How would you classify business activities?

Answer:

Business activities can be classified into two main categories: **industry** and **commerce**.

1. Industry:

Industry involves the production or processing of goods and materials.

It can be further divided into three categories:

• Primary Industry: Engages in extracting natural resources.

• Secondary Industry: Involves manufacturing and processing.

• Tertiary Industry: Provides support and services to the primary and secondary industries.

2. Commerce:

Commerce encompasses activities that facilitate the exchange of goods and services.

It is divided into two types:

• Trade: The buying and selling of goods and services.

• Auxiliaries to Trade: Activities that support trade, such as transportation, banking, insurance, warehousing, and advertising.

Question 5.

What are various types of industries?

Answer:

Meaning and Types of Industry

Definition of Industry: Industry refers to activities involving the growing, extracting, processing, fabricating, and constructing of useful products. It encompasses economic activities related to the extraction, production, and processing of goods.

Classification of Industrial Products:

1. Consumer Goods: Products used by the end consumers, such as edible oils, clothing, rice, sugar, televisions, scooters, and refrigerators.

2. Producers’ Goods: Items used to produce other goods, often capital goods, like machine tools and industrial machinery.

3. Intermediate Goods: Materials that are the finished products of one industry but serve as inputs for another, such as copper, which is used in making electrical gadgets, cables, and utensils.

Types of Industries:

1. Primary Industries: Involves extractive activities (like mining) and genetic industries (such as agriculture).

2. Secondary Industries: Includes manufacturing industries that convert raw materials into finished products, and construction industries that build infrastructure.

3. Tertiary Industries: Provide support services to primary and secondary industries, including transportation, banking, and insurance.

Question 6.

Explain any two business activities which are auxiliaries to trade.

Answer:

1. Transport and Communication:

Goods are often produced in specific regions (e.g., tea in Assam, cotton in Gujarat and Maharashtra), but they are needed across various parts of the country. Transport plays a crucial role in moving raw materials to production sites and finished products to consumers, overcoming geographical barriers through road, rail, or shipping.

Communication is equally important, as it allows producers, traders, and consumers to exchange information. Services like postal systems and telephone networks support business operations by facilitating this communication.

2. Banking and Finance:

Businesses require funds to acquire assets, purchase raw materials, and cover other operational expenses. Banks provide the necessary financial support through various services such as overdrafts, cash credits, loans, and advances.

Additionally, banks assist in the collection of cheques, the remittance of funds, and the discounting of bills. In international trade, banks help exporters collect payments from importers, and they also aid companies in raising capital from the public.

Question 7.

What is the role of profit in business?

Answer:

Role of Profit in Business

1. Incentive:

Profit is the primary motivator in business, driving individuals to work hard and take risks. The profit potential encourages people to start and sustain businesses, making risk-taking worthwhile.

2. Survival:

A business cannot continue without profit, as it needs to cover risks and operational costs. As Drucker stated, “Profit is the risk premium” necessary to maintain the business’s ability to produce and survive. Continuous losses can lead to the closure of the business.

3. Growth and Expansion:

Profit is essential for a business’s growth and future innovations. It provides internal funding for reinvestment, which is often more reliable than external sources. Profitability attracts additional capital, ensuring the business can diversify, modernize, and expand.

4. Prestige:

The reputation and goodwill of a business are often reflected in its ability to generate profit. A profitable business enjoys societal goodwill, whereas a loss-making one harms all stakeholders. Profitable businesses can also offer better wages and benefits to employees.

5. Measure of Efficiency:

Profit serves as a key indicator of business success and efficiency. It evaluates business performance and ensures the enterprise can cover future risks, maintain operations, and sustain its resource capacity. Additionally, profits provide a livelihood for business owners.

6. Return to Investors.

Investors expect a fair return on their capital, which is possible only if the business generates sufficient profits. This return encourages continued investment and supports the financial stability of the business.

Question 8.

What is Business risk? State its nature?

Answer:

Business Risk: Definition and Nature

Definition:

Business risk refers to the potential for inadequate profits or even losses due to uncertainties or unexpected events. For example, a shift in consumer preferences or increased competition might lead to a decline in demand for a product, causing business losses.

Nature of Business Risks:

1. Arising from Uncertainties:

Business risks stem from uncertainties, such as natural calamities, shifts in consumer preferences, price fluctuations, changes in government policies, and technological advancements. These uncertainties create risks because the outcomes of these future events are unpredictable.

2. Inherent in Every Business:

Every business faces some level of risk, and no business can completely avoid it. Although risk can be minimized through careful planning and management, it cannot be eliminated.

3. Varies with the Nature and Size of the Business:

The degree of risk varies depending on the nature and size of the business. For instance, businesses dealing in fashionable products face higher risks due to changing consumer tastes. Similarly, large-scale businesses often encounter higher risks compared to smaller ones due to their larger scope and complexity.

4. Profit as a Reward for Risk-Taking:

The principle “no risk, no gain” is fundamental in business. The greater the risk, the higher the profit potential. Entrepreneurs take on risks with the expectation of earning profits, which serve as the reward for their risk-taking efforts.

Long Answer Questions: Nature and Purpose of Business

Question 1.

Explain the characteristics of the business.

Answer:

The nature of a business can be better understood by examining its key characteristics:

1. Dealing in Goods and Services:

Business activities revolve around the sale or exchange of goods and services. These goods may be:

• Consumer Goods: Items like bread, cold drinks, and sugar.

• Capital Goods: Tools, machinery, etc.

Services include essentials like water, electricity, gas, insurance, and transportation.

2. Production and Distribution:

Business encompasses activities related to the production and distribution of goods and services.

• Production: Involves converting raw materials into finished products.

• Distribution: Facilitates the transfer of goods from producers to consumers.

Businesses include industrial undertakings, trading firms, and service organizations like banking, transport, warehousing, and insurance.

3. Creation of Utility:

Business enhances the usefulness of goods and services to meet human needs:

• Form Utility: Created by converting raw materials into finished goods.

• Place Utility: Created by transporting goods from production to consumption locations.

• Time Utility: Created by storing goods for future use and making them available when needed.

4. Satisfaction of Customer Needs:

The primary goal of business activities is to satisfy customer needs.

Production for personal use is not considered a business. For example, making food at home for personal consumption isn’t business, but preparing food for others in a restaurant for payment is.

5. Regular Dealings:

Business involves continuous transactions. There should be regularity in the exchange of goods and services for money. A one-time transaction doesn’t constitute a business. For example, selling a single motorbike for profit is not a business, but regularly buying and selling motor vehicles for income is.

6. Profit Motive:

The primary objective of business is to earn profit. Profits are essential for the survival and growth of the business. Any activity conducted without the intention of making a profit cannot be considered a business.

7. Risk and Uncertainty:

Business involves risk due to uncertainties such as:

• Technology Changes: May require new machinery.

• Changing Consumer Preferences: Can decrease demand.

• Increased Competition: May reduce market share.

• Resource Shortages: Such as raw materials or power.

• External Risks: Including natural calamities, theft, and fire.

• Businesses face risks related to labour relations, government policies, and management decisions.

• Economic Activity: Business is fundamentally an economic activity aimed at producing and distributing goods and services to earn profits.

Question 2.

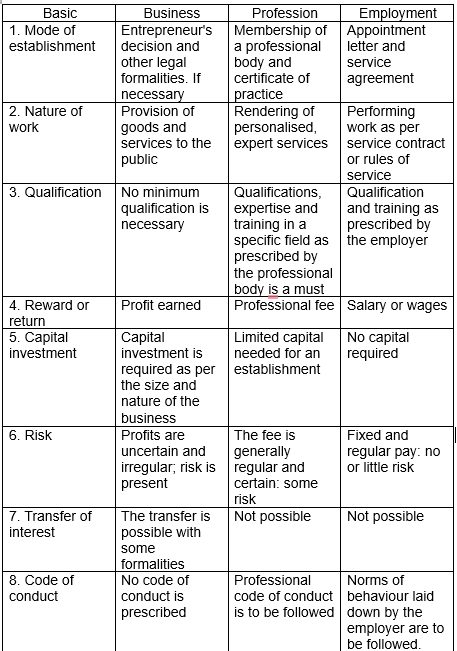

Compare business with profession and employment.

Answer:

Question 3.

Explain with examples the various types of industries.

Answer:

Types of Industries

Industries play a crucial role in the production of goods through the use of various resources. Production encompasses all processes that lead to the creation of products that satisfy human wants, from the growing of crops and processing of materials to the construction of infrastructure. The purpose of industry is to apply factors of production to make them suitable for consumption or use. This includes everything from farming and animal breeding to the fabrication of parts and construction of bridges.

Types of Industries

1. Genetic Industries: These industries are involved in the reproduction or multiplication of plant and animal species. They focus on growing and breeding various organisms.

Examples include:

• Nurseries: Growing plants for sale.

• Poultry Farms: Raising birds for meat and eggs.

• Animal Husbandry: Rearing cattle for milk, sheep for wool, and other breeding farms.

• Pisciculture: Cultivating fish in ponds and rivers.

• Orchards: Growing fruits.

• Agriculture: Growing crops.

2. Extractive Industries: These industries extract natural resources from the earth, sea, or air. They involve obtaining raw materials directly from nature, such as:

• Mining: Extracting minerals from the earth.

• Fishing: Harvesting fish from water bodies.

• Quarrying: Extracting stone and other materials from quarries.

• Forestry: Procuring timber and wood products from forests.

• Hunting: Collecting wildlife.

Extractive industries are among the oldest and provide raw materials for other industries. They differ from genetic industries as they do not add to the wealth extracted; they only collect resources.

3. Manufacturing Industries: These industries transform raw and semi-finished materials into finished products. They create utility by changing the shape and form of materials. Types include:

• Analytical Manufacturing: Separating raw materials into various products. For example, an oil refinery produces petrol, diesel, and kerosene from crude oil.

• Synthetical Manufacturing: Combining materials to create new products. For example, making cement from concrete, gypsum, and coal.

• Processing Manufacturing: Transforming raw materials through various stages. For example, turning cotton into cloth through spinning, weaving, dyeing, and printing.

• Assembling Manufacturing: Combining parts to create a final product. For example, assembling radios, TV sets, and watches.

4. Construction Industries: These industries focus on building infrastructure such as buildings, bridges, roads, and dams. They utilize products from manufacturing industries, such as bricks and steel, to create durable structures. Construction products remain fixed in one location and cannot be moved to the market for sale.

Other Classifications

• Primary Industries: This term encompasses genetic and extractive industries that provide raw materials.

• Secondary Industries: This includes manufacturing and construction industries that process or build upon raw materials.

By Scale of Operations

• Large-Scale Industries: These industries use capital-intensive techniques and employ large amounts of capital. They include industries like steel production and machinery manufacturing.

• Small-Scale Industries: These use less capital and often focus on consumer products like cosmetics, stationery, and food items.

By Capital Investment

• Heavy Industries: Involve significant investment and produce capital goods, such as steel, machinery, and ships.

• Light Industries: Require less capital and produce consumer goods, such as food products, jewellery, and cosmetics.

Tertiary Industries

These industries provide essential services that support the functioning of the economy. They include transport, banking, insurance, warehousing, and advertising. Tertiary industries bridge the gap between producers and consumers and address issues in the production and distribution of goods and services.

Question 4.

Describe the activities relating to commerce.

Answer:

• Commerce Activities

Commerce involves the distribution of goods and services, encompassing two primary types of activities: trade and auxiliaries to trade.

• Trade

Trade is a fundamental component of commerce, encompassing the sale, transfer, or exchange of goods. It ensures that products reach consumers efficiently. With the scale of modern production, it is impractical for producers to directly reach individual buyers. Therefore, businessmen act as intermediaries to facilitate the distribution of goods across various markets. Without trade, large-scale production would be unfeasible.

Trade can be classified into two main categories:

1. Internal Trade: Also known as domestic or home trade, this involves the buying and selling of goods within a country. It is further divided into:

• Wholesale Trade: Involves the purchase and sale of goods in bulk, typically to retailers or other wholesalers.

• Retail Trade: Involves the sale of goods in smaller quantities directly to the end consumers.

2. External Trade: Also known as foreign trade, this involves the exchange of goods and services between countries. It includes:

• Import Trade: Purchasing goods from other countries.

• Export Trade: Selling goods to other countries.

• Entrepot Trade: Importing goods for re-exporting them to other countries.

Auxiliaries to Trade:

Auxiliaries to trade are activities that support and facilitate trade. These services enhance the efficiency of a trade by addressing various challenges related to the production and distribution of goods. Key auxiliaries include:

1. Transport: Facilitates the movement of goods from one location to another, enabling efficient distribution across regions.

2. Banking: Provides financial services, including loans and credit, to manufacturers and traders, supporting their operations and growth.

3. Insurance: Offers coverage for various business risks, protecting against potential losses and uncertainties.

4. Warehousing: Provides storage facilities, creating time utility by allowing goods to be stored until they are needed, thus ensuring a steady supply.

5. Advertising: Helps in promoting goods and services by providing information to consumers, thereby facilitating sales and market reach.

These auxiliaries are integral to commerce and play a crucial role in overcoming obstacles related to production, distribution, and consumption. They support the smooth functioning of trade by ensuring efficient movement, financing, risk management, storage, and promotion of goods.

Question 5.

Why does a business need multiple objectives? Explain any five Economic and Social objectives of Business.

Answer:

A business requires multiple objectives to ensure balanced growth and sustainable success. With various goals, a business can address different aspects of its operations, from production to customer satisfaction.

Objectives help define specific targets, such as sales goals, capital requirements, and production quantities. They also provide a framework for evaluating performance and making improvements. Since businesses operate within a society and are influenced by external factors, having multiple objectives helps them address both economic and social aspects effectively.

Economic Objectives

1. Market Standing: Market standing refers to a business’s position relative to its competitors. To achieve strong market standing, a business must offer competitive products and services that satisfy customer needs. Maintaining a solid market position ensures the business can compete effectively and grow in its sector.

2. Innovation: Innovation involves introducing new ideas, methods, or products. It can be divided into:

Product or Service Innovation: Developing new products or improving existing ones.

Process Innovation: Enhancing the methods used to deliver products or services.

Innovation is crucial for staying relevant and competitive in a dynamic market.

3. Productivity: Productivity measures the efficiency of turning inputs into outputs. It is calculated by comparing the value of output with the value of input. A business must focus on increasing productivity to optimize resource use and achieve better performance and growth.

4. Physical and Financial Resources: Businesses need physical resources like machinery and buildings, as well as financial resources to operate effectively. Acquiring and efficiently utilizing these resources is essential for production and service delivery.

5. Earning Profits: Profitability is a key objective for any business. Earning profits ensures the financial health of the business and supports its survival and expansion. Profitability is assessed by comparing profits with capital investment.

Social Objective

1. Manager Performance and Development: Effective management is

crucial for business success. Companies should invest in programs to enhance managerial skills and performance, ensuring that managers are motivated and capable of leading the organization effectively.

2. Worker Performance and Attitude: Workers’ performance and attitudes significantly impact productivity and profitability. Businesses should aim to improve worker performance and foster a positive work environment to enhance overall efficiency and job satisfaction.

3. Social Responsibility: Businesses have a responsibility to contribute to social welfare and address social issues. This includes acting ethically, supporting community initiatives, and working to improve societal conditions.

4. Providing Employment: Creating job opportunities is a critical social objective, especially in regions with high unemployment. By generating employment, businesses contribute to economic stability and improve the quality of life for individuals.

5. Prevention of Pollution: As industries grow, pollution becomes a serious concern. Businesses should implement measures to reduce environmental impact and prevent pollution, thereby contributing to a healthier environment.

Additional Considerations for Business Planning:

1. Type of Business: Entrepreneurs should choose a business type based on market potential, technical knowledge, and customer needs.

2. Size of the Firm: The scale of operations should align with market demand and available capital. A large-scale operation may be suitable for stable markets, while a smaller scale might be preferable in uncertain conditions.

3. Choice of Form of Ownership: The form of ownership (e.g., sole proprietorship, partnership, joint-stock company) affects factors like capital requirements, liability, and continuity. Choosing the right form depends on the business’s specific needs and goals.

4. Location of Business: The location affects production costs, access to resources, and customer service. Factors such as raw material availability, labour, and infrastructure should be considered when selecting a location.

5. Financing: Proper financial planning is essential for acquiring and utilizing capital. This involves determining capital requirements, sourcing funds, and managing investments.

6. Physical Facilities: Adequate facilities, including machinery and buildings, are necessary for efficient operations. The choice of physical facilities should align with the business’s nature and scale.

7. Plant Layout: A well-designed plant layout optimizes the arrangement of machinery and equipment, enhancing production efficiency and workflow.

8. Competent Workforce: Recruiting and training skilled workers is vital for converting resources into desired outputs. Effective workforce management ensures high performance and productivity.

9. Tax Planning: Understanding and planning for tax liabilities is crucial for financial management. Tax planning helps in making informed business decisions and managing tax impacts.

10. Launching the Enterprise: Once planning is complete, launching the business involves mobilizing resources, completing legal requirements, starting production, and promoting sales.

These considerations help in establishing a solid foundation for business operations and achieving long-term success.

Question 6.

Explain the concept of business risk and its causes.

Answer:

Business activities are inherently uncertain and are exposed to various risks arising from economic, natural, physical, and human factors.

According to C.O. Hardy, “Business risks may be defined as uncertainty regarding cost, loss, or damage.” Wheeler describes risk as “the chance of loss, the possibility of some unfavourable occurrence.”

Causes of Business Risks:

Business risks stem from several causes, which can be categorized as follows:

1. Natural Causes: Natural events are significant contributors to business risks, often beyond human control. Disasters such as floods, droughts, famines, earthquakes, volcanic eruptions, lightning, snowstorms, hailstorms, tides, and epidemics can lead to severe loss of life, property, and income. Even the death of a business owner or partner can result in the closure of a business. Since these natural causes are uncontrollable, they pose significant risks to businesses.

2. Human Causes: Human actions are crucial sources of business risks. Negligence or carelessness by employees can lead to accidents or fires, causing significant damage to life and property. Losses can also occur due to spoilage, breakage, or errors in estimating product demand. Strikes or lockouts can arise from pride, prejudice, or poor management decisions. Inefficient management, irrational decision-making, and human failures, such as those that led to the downfall of Enron Corporation in the U.S.A., are also sources of business risk.

3. Economic Causes: Economic causes are related to fluctuations in market conditions. Changes in demand and pricing, the availability of cheaper substitutes, and intense competition can all negatively impact a business. For example, the advent of colour televisions displaced black-and-white TVs from the market.

4. Physical and Technical Causes: Business risks can also arise from physical and technical issues. Technological advancements may render machinery obsolete before its anticipated lifespan ends. Mechanical failures, such as boiler explosions or gas leaks, can cause severe damage. Assets may depreciate due to shrinkage, loss of weight, or vaporization. Additionally, power failures or transportation issues can disrupt business operations, leading to financial losses.

5. Political and Legal Causes: Changes in government policies, such as those related to foreign trade, multinational collaborations, licensing, and taxation, can also create business risks. A business may suffer losses due to import and export restrictions, exchange rate fluctuations, or government controls on the production and distribution of certain products. Therefore, political and legal changes are important sources of business risk.

Additional One Mark Questions and Answers: Nature and Purpose of Business

Question 1.

What is Economic Activity?

Answer:

Human activities performed in exchange for money or money’s worth are called economic activities.

Question 2.

Name any one type of economic activity.

Answer:

Business

Question 3.

What is Business?

Answer:

Business refers to an occupation where people regularly engage in activities related to the purchase, production, and/or sale of goods and services to earn profits.

Question 4.

Write any one characteristic of business activity.

Answer:

Economic activity

Question 5.

Mention the two broad categories of business activity.

Answer:

Industry and Commerce

Question 6.

Name any one type of Primary Industry.

Answer:

Extractive industry

Question 7.

Name any one type of Secondary Industry.

Answer:

Manufacturing

Question 8.

Give an example of Extractive Industries.

Answer:

Mining

Question 9.

Give an example of Genetic Industries.

Answer:

Poultry farming

Question 10.

Give an example of Manufacturing Industries.

Answer:

Sugar Industry

Question 11.

Give an example of Construction Industries.

Answer:

Construction of dams

Question 12.

What is Trade?

Answer:

Trade refers to the buying and selling of goods.

Question 13.

What do you mean by Auxiliary to Trade?

Answer:

Activities that assist trade are known as auxiliaries to trade.

Question 14.

Mention any one objective of business.

Answer:

A source of income for a business person.

Question 15.

Give an example of the Service Industry.

Answer:

Transport

Question 16.

What do you mean by the hindrance of trade?

Answer:

Obstacles that a businessperson faces while conducting business or trade activities are termed hindrances of trade.

Question 17.

State any one type of hindrance to trade.

Answer:

Hindrance of Place

Question 18.

State any one type of business risk.

Answer:

Operational risk

Question 19.

What is meant by Non-Economic Activity?

Answer:

Non-economic activities are those performed out of love, sympathy, sentiments, patriotism, etc.

Question 20.

Give an example of a Non-Economic Activity.

Answer:

A worker volunteering in a factory.

Question 21.

Give an example of a Profession.

Answer:

Lawyer

Question 22.

Give an example of an Analytical Industry.

Answer:

Processing crude oil into petrol, diesel, kerosene, etc.

Question 23.

Give an example of the Synthetic Industry.

Answer:

Cement production by mixing concrete, gypsum, and coal.

Question 24.

Give an example of the Processing Industry.

Answer:

Textile industry

Question 25.

Give an example of the Assembly-Line Industry.

Answer:

Vehicle Manufacturing

Two Marks Questions and Answers: Nature and Purpose of Business

Question 1.

Define Business.

Answer:

According to L.H. Haney, “Business may be defined as human activity directed towards producing or acquiring wealth through the buying and selling of goods.”

Question 2.

What is a Profession?

Answer:

A profession is an occupation, practice, or vocation that requires mastery of a complex set of knowledge and skills, typically gained through formal education and/or practical experience.

Question 3.

What is Employment?

Answer:

Employment refers to work or activities in which a person receives valuable consideration, usually in the form of wages or salary.

Question 4.

What is Industry?

Answer:

Industry encompasses economic activities connected with the conversion of resources into useful goods.

Question 5.

What is Commerce?

Answer:

Commerce involves all activities necessary for facilitating the exchange of goods and services.

Question 6.

What do you mean by Extractive Industries?

Answer:

Extractive industries involve processes that extract raw materials from the earth for consumer use, such as mining for metals, minerals, and aggregates.

Question 7.

What do you mean by Genetic Industries?

Answer:

Genetic industries focus on the reproduction and multiplication of certain species of plants and animals for sale.

Question 8.

What do you mean by Manufacturing Industries?

Answer:

Manufacturing industries are engaged in transforming raw materials into finished products using machinery and human labour.

Question 9.

What do you mean by Constructive Industries?

Answer:

Constructive industries are involved in building infrastructure such as buildings, bridges, roads, dams, and canals. Unlike other industries, these products are typically constructed on-site.

Question 10.

What do you mean by Tertiary/Service Industries?

Answer:

The service industry, also known as the tertiary sector, plays a vital role in national development by providing essential services like transport, banking, and healthcare.

Question 11.

Write the meaning of Business Risks.

Answer:

Business risks refer to the possibility of inadequate profits or losses due to uncertainties or unexpected events.

Question 12.

State any two causes of Business Risks.

Answer:

• Natural Causes

• Human Causes

Question 13.

What are Analytical Industries?

Answer:

Analytical industries involve analysing and separating different elements from the same material, such as oil refining.

Question 14.

What are Synthetic Industries?

Answer:

Synthetic industries combine various ingredients to create new products, such as in cement production.

Question 15.

What are Processing Industries?

Answer:

Processing industries involve the transformation of materials or data through a series of stages to achieve a specific result, like in the textile industry.

Question 16.

What are Assembly-Line Industries?

Answer:

Assembly-line industries focus on assembling different parts to create a new product, such as in vehicle manufacturing.

Question 17.

State any two types of Business Risks.

Answer:

• Financial Risk

• Operational Risk

Question 18.

Name any two Auxiliaries to Trade.

Answer:

• Transport and Communication

• Banking and Finance

Question 19.

How do you overcome the hindrance of person and finance?

Answer:

Banking helps overcome the hindrance of finance, while transport and communication help overcome the hindrance of a person.

Question 20.

How do you overcome the hindrance of place and trade?

Answer:

Advertising, transport, and communication help overcome the hindrance of place and trade.

Question 21.

How do you overcome the hindrance of risk and knowledge?

Answer:

Warehousing helps overcome the hindrance of risk, and advertising helps overcome the hindrance of knowledge.

Question 22.

Give any two examples of Service Industries.

Answer:

• Hotel

• Hospital

Question 23.

What is meant by Entrepot Trade?

Answer:

Entrepot trade refers to the practice of importing goods and then re-exporting them, sometimes with additional processing or repackaging.

Question 24.

State any two Economic Objectives of Business.

Answer:

• Market Standing

• Innovation

Question 25.

State any two Social Objectives of the Business.

Answer:

• Social Responsibility

• Prevention of Pollution

Five Marks Question and Answer: Nature and Purpose of Business

Question 1:

Briefly Explain the Classification of Business Activities.

Answer:

Human activities performed in exchange for money or its equivalent are termed economic activities. These activities can be classified into three main categories: Profession, Employment, and Business.

1. Profession:

A profession is an occupation undertaken by individuals with specialized skills and knowledge, such as doctors, lawyers, engineers, and accountants. Professionals provide specialized services to clients in exchange for fees. To become a professional, one must acquire specific qualifications and expertise in their field. The hallmark of a profession is the application of learned knowledge and skills to solve problems or offer advice in return for compensation.

2. Employment:

Employment refers to an occupation in which an individual offers their services to another person or organization in exchange for a salary or wage. In this relationship, the person who hires is known as the employer, while the person who is hired is referred to as the employee or worker. Employment is characterized by a contract or agreement, where the employee agrees to perform certain tasks under the direction of the employer.

3. Business:

Business is an economic activity focused on the production, distribution, and exchange of goods and services with the primary goal of earning a profit. It encompasses all activities directly or indirectly related to producing, purchasing, and selling goods and services.

A business can involve manufacturing products, providing services, or engaging in trade, and its main objective is to generate profit by meeting the needs and wants of consumers.

Question 2:

Briefly Explain the Economic Objectives of the Business.

Answer:

The economic objectives of a business focus on its financial success and sustainability. These include:

1. Profit Earning:

The primary goal of any business is to earn profit, which is crucial for its survival, growth, and ability to take on future risks.

2. Customer Creation:

A business needs customers to thrive. Offering quality products or services at reasonable prices helps attract and retain customers, ensuring consistent revenue.

3. Innovation:

Innovation involves improving products, production processes, or distribution methods. This helps businesses reduce costs, enhance quality, and attract more customers.

4. Optimal Resource Use:

Businesses must efficiently use resources like labour, materials, and capital. Optimal resource management helps minimize costs and maximize profits.

5. Capital Management:

Proper management of capital is essential for purchasing resources, covering operational costs, and ensuring the business runs smoothly.

As you know, to run any business you must have sufficient capital or funds. The amount of capital may be used to buy machinery, and raw materials, employ men, and have the cash to meet day-to-day expenses.

Question 3.

Briefly explain the Types of Industries.

Answer:

Types of Industries

Industries are classified into various types based on the nature of their activities. The main types of industries are as follows:

1. Primary Industry:

These industries are directly related to nature and focus on producing goods with the help of natural resources. Examples include agriculture, farming, forestry, fishing, and horticulture.

A. Genetic Industry:

Genetic industries are involved in the reproduction and multiplication of certain species of plants and animals for sale. Examples include plant nurseries, poultry farming, and cattle breeding.

B. Extractive Industry:

This type of industry extracts goods from natural sources such as soil, air, or water. The products are typically raw materials used by other industries. Examples include mining, oil extraction, and the collection of timber or rubber from forests.

2. Secondary Industry:

These industries take raw materials produced by primary industries and convert them into finished goods.

A. Manufacturing Industry:

Manufacturing industries use machines and labour to transform raw materials into final products, which can be consumer or producer goods. Examples include the textile, chemical, sugar, and paper industries.

B. Construction Industry:

The construction industry focuses on building structures such as buildings, bridges, roads, dams, and canals. Unlike other industries, the goods produced by the construction industry are created and used in the same location.

3. Tertiary or Service Industry:

This industry provides services rather than physical goods. Key sectors include hospitality, tourism, and entertainment.

Question 4.

Briefly explain the Types of Manufacturing Industry

Answer:

Types of Manufacturing Industry:

Manufacturing involves the conversion of raw materials into semi-finished or finished products. Examples include the paper and steel industries. Manufacturing industries are classified into the following types:

1. Analytical Industry:

In this type, different products are derived from the same raw material. Example: Refining crude oil to produce petrol, diesel, and other products.

2. Synthetic Industry:

Multiple raw materials are combined to create a new product.

Example: Cement is made by mixing limestone, gypsum, coke, and other materials.

3. Processing Industry:

Raw materials are processed through several stages to produce the final product.

Example: Manufacturing of sugar and paper involves multiple stages of processing.

4. Assembly Industry:

Pre-produced components are assembled to form a new product. Example: The automobile and PC manufacturing industries.

Ten Marks Questions Nature and Purpose of Business

Question 1.

What do you mean by trade explain its Types.

Answer:

Trade and Its Types

Trade refers to the buying and selling of goods and services in exchange for money or its equivalent. It involves the transfer of goods and services from one person or entity to another. Trade can be classified into the following two types:

A. Internal Trade:

Also known as home trade, internal trade occurs within the geographical boundaries of a country. It is further divided into two categories:

• Wholesale Trade:

Involves purchasing goods in large quantities from producers or manufacturers and selling them in bulk to retailers, who then sell them to consumers.

• Retail Trade:

Involves buying goods in smaller quantities from wholesalers and selling them in smaller amounts directly to consumers for personal use.

B. External Trade:

Also called foreign trade, external trade refers to the buying and selling of goods between two or more countries. It includes the following types:

• Export Trade:

When a trader from one country sells goods to a trader in another country.

Example: A trader from India sells goods to a trader in China.

• Import Trade:

When a trader in one country purchases goods from a trader in another country.

Example: A trader from India purchases goods from a trader in China.

• Entrepot Trade:

This occurs when goods are imported from one country, undergo some processing or modifications, and are then re-exported to another country.

Question 2.

Briefly explain the type of business risks.

Answer:

Types of Business Risks

Business risks refer to the uncertainties in profits or the possibility of loss due to unforeseen events that may cause a business to fail. These risks can be classified into the following types:

1. Strategic Risk:

These risks are related to the overall operations of a specific industry and arise from factors such as:

• Changes in the business environment

• Transaction-related risks

• Investor relations

2. Financial Risk:

These risks are associated with the financial structure, management, and transactions within a business. It includes risks related to cash flow, funding, and debt management.

3. Operational Risk:

This refers to risks related to the internal processes, operations, and administrative procedures of the business. It includes failures in systems, supply chains, or human resources.

4. Compliance Risk (Legal Risk):

These risks arise from the need to comply with laws, regulations, and government policies. Non-compliance could result in fines, penalties, or legal action.

5. Other Risks:

These include risks from external factors like natural disasters (floods, earthquakes) or other unforeseen events, depending on the nature and scale of the business.

Question 3.

Briefly explain the aids or auxiliaries to trade

Answer:

Aids or Auxiliaries to Trade

Aids or auxiliaries to trade refer to the activities that facilitate the smooth movement of goods from production centres to consumption centres. These can be categorized into five key areas:

1. Transportation:

It is not possible to sell all goods at the production centres, so they need to be transported to different locations where there is demand. Transportation refers to the movement of people and goods from one place to another.

2. Warehousing:

In an era of mass production, storing goods is essential until they are sold. Warehouses, also known as go-downs, ensure that goods are stored safely from the time of production until they reach the market.

3. Insurance:

Goods can be lost or damaged during production, transit, or storage due to accidents, fires, theft, or other risks. Insurance protects businesses from these risks by compensating for losses. To get this coverage, businesses take out insurance policies and pay premiums.

4. Advertising:

Advertising plays a crucial role in promoting goods. It allows producers to inform potential customers about their products and create demand. Advertising can be done in various ways, including indoor and outdoor methods.

5. Banking:

Banks are financial institutions that accept public deposits and lend money to those in need. They provide a range of services that are essential for business activities, including handling transactions, offering loans, and managing finances.